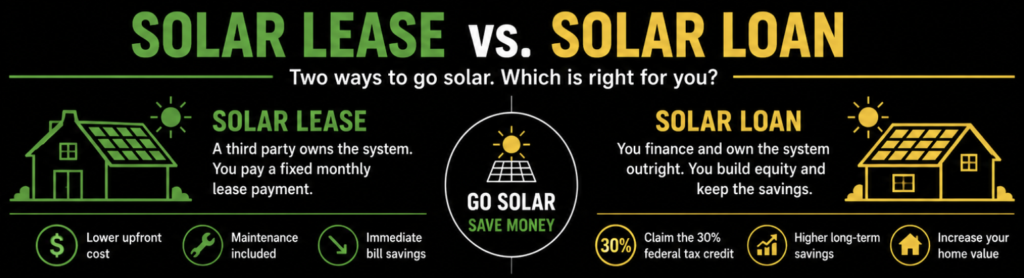

A solar loan allows homeowners to finance and own their solar system outright, making them eligible for the 30% federal tax credit and maximum long-term savings. A solar lease allows a third party to own the system while the homeowner makes monthly payments for the benefits of solar energy, typically with lower upfront costs but fewer ownership benefits.

Neither option is universally better. The right choice depends on your financial goals, how long you plan to stay in your home, whether you have tax liability to offset, and how much weight you place on ownership versus simplicity. This guide walks through how each option works, what it costs, and which type of homeowner each tends to fit best.

Solar Lease vs. Solar Loan

Solar loan: You borrow money to purchase the solar system. The system is yours from day one. You claim the federal tax credit, build equity, and own an asset that increases your home’s value. Monthly loan payments replace your electricity bill, and once the loan is paid off, the energy your system produces is effectively free.

Solar lease: A third-party company owns the solar panels on your roof. You pay a monthly lease payment for the right to use the energy the system produces. The company handles maintenance. You benefit from reduced electricity costs without taking on system ownership, but the tax credit and long-term asset value go to the system owner, not you.

Both options allow you to go solar with little or no money down. The difference is in who owns the system, who benefits from the incentives, and how the long-term economics shake out.

How Does a Solar Loan Work?

A solar loan works like most business or home improvement financing. You borrow money from a lender to purchase your solar system, then repay the loan over time with interest. Loan terms typically range from 5 to 25 years, and current interest rates for solar loans in 2025 range from approximately 4.5% to 9% depending on the lender, loan term, and your credit profile.

Because you own the system from day one, you are eligible for the 30% federal solar tax credit, which reduces your net system cost by 30% at tax time. On a $28,000 system, that is $8,400 back, reducing your effective cost to $19,600. This is one of the most significant financial advantages of ownership over leasing.

When structured correctly, the monthly loan payment is designed to be equal to or less than the electricity costs the system offsets, which means you can start saving from month one without increasing your overall monthly expenses. Once the loan is paid off, your energy costs drop dramatically because you own a producing asset with no ongoing payments.

Advantages of Solar Loans

- You own the system. Ownership means you build equity, just like a home improvement, and the system adds value to your property.

- You claim the tax credit. The 30% federal Investment Tax Credit goes to the system owner. With a loan, that is you.

- Higher long-term savings. Once the loan is paid off, the energy your system produces costs you nothing. That is typically 10 to 20 years of ownership where your electricity expenses are dramatically reduced.

- Rising utility rates work in your favor. As Duke Energy rates increase, the value of your system’s production grows. An owned system benefits fully from that appreciation.

- No third-party equipment on your roof. You control your system, your monitoring, and your decisions about upgrades or changes.

Potential Drawbacks of Solar Loans

- Interest adds to total cost. Depending on your rate and term, interest payments mean you pay more than the system’s sticker price over the life of the loan.

- Credit requirements. Most solar loans require a minimum credit score, typically 640 to 700 or higher depending on the lender and loan type.

- You are responsible for maintenance. As the system owner, any maintenance costs beyond the manufacturer warranty period are your responsibility. Most quality systems require very little maintenance over their lifespan.

How Does a Solar Lease Work?

Under a solar lease, a solar company installs panels on your roof at little or no upfront cost. They own the equipment, maintain it, and monitor its performance. You pay a fixed monthly lease payment in exchange for the right to use the energy the system produces. Programs like LightReach through Palmetto Solar are examples of how lease programs are structured in the current NC market.

Lease terms typically run 20 to 25 years. Monthly payments are designed to be lower than your current electric bill, so you see immediate savings. The company that owns the system handles any maintenance or repair issues that arise during the lease period, which appeals to homeowners who want the benefits of solar without the responsibilities of ownership.

A variation on the lease is the Power Purchase Agreement (PPA), where instead of paying a fixed monthly amount, you pay per kilowatt-hour for the energy the system produces, typically at a rate below your utility’s retail rate.

Advantages of Solar Leases

- Low or no upfront cost. Most lease programs require little to nothing down, making solar accessible to homeowners who do not want to finance a purchase.

- Immediate bill reduction. Lease payments are structured to be lower than your current electricity costs from the start.

- Maintenance is handled. The system owner manages monitoring, maintenance, and repairs throughout the lease term.

- Production guarantees. Many lease programs include a minimum production guarantee, compensating you if the system underperforms.

- Simpler decision. No loan to qualify for, no tax credit to manage, no ownership responsibilities to navigate.

Potential Drawbacks of Solar Leases

- You do not own the system. The solar company owns the panels on your roof. You are a customer, not an owner.

- The tax credit goes to the leasing company. Because they own the system, they claim the 30% federal tax credit, not you.

- Long-term savings are lower. Once a loan is paid off, your energy is effectively free. With a lease, you are still making payments for the life of the agreement.

- Home sale complications. Selling a home with a leased solar system requires either transferring the lease to the buyer or buying out the lease. Some buyers are hesitant about assuming a lease obligation.

- Rate escalators. Some lease agreements include annual payment increases. Always review the escalator clause before signing.

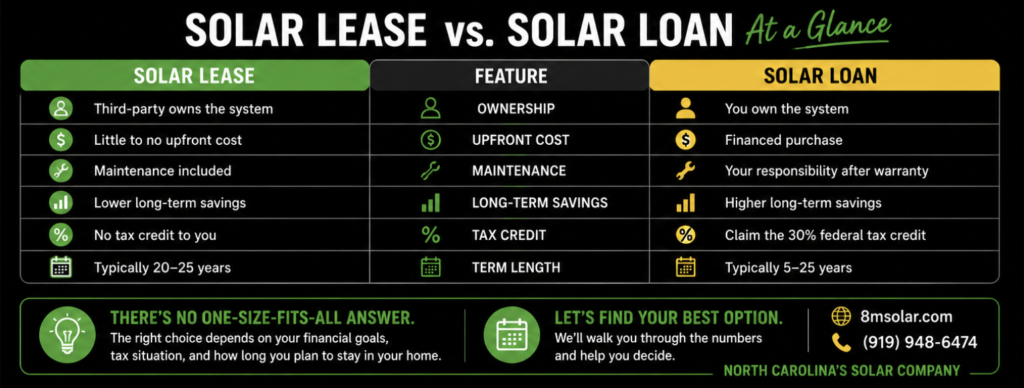

Solar Lease vs. Solar Loan: Side-by-Side Comparison

| Feature | Solar Loan | Solar Lease |

| Who owns the system? | You | Third-party company |

| Federal tax credit (30% ITC) | You claim it | Leasing company claims it |

| Upfront cost | Low to none (financed) | Low to none |

| Monthly payments | Loan payment (replaces electric bill) | Lease payment (replaces electric bill) |

| Maintenance responsibility | Homeowner (after warranty) | Leasing company |

| Home value impact | Positive (owned asset) | Neutral to complicated |

| Long-term savings potential | Higher (no payment after payoff) | Moderate (payments continue) |

| Home sale process | Standard | Requires lease transfer or buyout |

| Credit requirements | Yes (varies by lender) | Minimum score (often 660+) |

| System ownership at end of term | You own it outright | Leasing company owns it |

Which Option Saves More Money?

Over a full system lifespan, a solar loan generally produces greater total savings than a lease. The reasons are straightforward: you claim the federal tax credit, you build equity in a home asset, and once the loan is paid off, the energy your system produces comes at no ongoing cost. A lease means you are still making payments 15 or 20 years after installation.

That said, the gap between the two options is not always as large as it appears on paper, and short-term cash flow considerations matter. For homeowners who are focused on immediate monthly savings and do not have significant tax liability to offset with the ITC, the difference in total return may be smaller than expected.

The honest answer is that savings depend on your specific situation. The best way to compare your options is with an actual financial model based on your energy usage, your tax situation, and the specific loan terms or lease terms available to you. That is a conversation worth having with an experienced local installer rather than resolving with a general rule.

Who Should Consider a Solar Loan?

Homeowners Seeking Maximum Savings

If your primary goal is to minimize the total amount you spend on electricity over the next 25 years, a loan is typically the better path. Once the loan is paid off, your solar savings in North Carolina continue with no ongoing payment obligation.

Homeowners Planning to Stay Long-Term

The financial return from solar ownership improves with time. Homeowners who plan to stay in their homes for 10 or more years capture more of the post-payoff savings period and benefit fully from the asset they have built.

Homeowners Who Want Ownership

If you want full control of your energy system, the ability to modify or expand it on your own terms, and the property value benefits of a owned solar installation, a loan is the right structure. Ownership also simplifies the home sale process compared to a lease transfer.

Homeowners With Tax Liability to Offset

The 30% federal tax credit is only valuable if you have sufficient tax liability to use it. Homeowners who owe significant federal taxes in the year of installation benefit most from ownership. If your annual federal tax bill is low, the ITC advantage shrinks, which changes the loan vs. lease comparison.

Who Should Consider a Solar Lease?

Homeowners Prioritizing Low Upfront Cost and Simplicity

Lease programs are designed to make solar as simple as possible. If your primary goal is to reduce your electricity bill without navigating loan qualifications, tax credit claims, or ownership responsibilities, a lease accomplishes that with minimal friction.

Homeowners Focused on Immediate Bill Reduction

Lease payments are structured to be lower than current electric bills from month one. For homeowners who are primarily focused on improving monthly cash flow rather than long-term return, the lease structure delivers that outcome without requiring a loan.

Homeowners With Limited Tax Liability

If you would not be able to use the 30% ITC because your federal tax bill is too low, one of the primary advantages of ownership diminishes. In that scenario, the gap between a loan and a lease narrows, and the simplicity of a lease becomes relatively more attractive.

What About Prepaid Solar Leases?

A prepaid solar lease is a variation on the standard lease structure where instead of making monthly payments over the lease term, the homeowner pays a single lump sum upfront to cover the full cost of the lease. In exchange, the homeowner benefits from solar energy production for the lease period with no ongoing monthly obligations.

Prepaid leases can make sense in specific situations, particularly for homeowners who want to avoid monthly payments, do not want to take on a loan, and are comfortable with the third-party ownership structure. The upfront cost is typically lower than purchasing the system outright, though it is higher than a standard lease’s monthly payment structure.

The ownership considerations are the same as a standard lease: the solar company still owns the system, and the tax credit still goes to them rather than you. Whether a prepaid lease makes financial sense compared to a loan or outright purchase depends on the specific terms, your tax situation, and your goals. It is worth modeling all three options before deciding.

Are Solar Loans and Leases Still Worth It in 2025?

Yes, for most North Carolina homeowners. The fundamentals that make solar financially attractive remain firmly in place regardless of which financing path you choose:

- Utility rates are rising. Duke Energy has been increasing rates steadily, and that trend is expected to continue. Solar insulates you from those increases regardless of whether you own or lease.

- The 30% federal tax credit remains available through 2032. Homeowners who own their systems through a loan or cash purchase can claim this significant incentive.

- Systems last 25 to 30 years. The long lifespan of modern solar panels means the financial return compounds significantly over time, regardless of financing structure.

- Energy independence has real value. Paired with battery backup systems, solar provides resilience against outages and grid disruptions that a utility-only household cannot match.

How 8MSolar Helps Homeowners Compare Financing Options

At 8MSolar, we offer multiple solar financing options for NC homeowners, including solar loans, cash purchase, and lease programs like LightReach. We do not push one financing path over another. We help you understand what each option actually means for your monthly cash flow, your long-term savings, your tax situation, and your home.

Here is what that process looks like:

- Personalized savings analysis. We model your savings under each financing scenario based on your actual energy usage and Duke Energy rates, not national averages.

- Tax credit consultation. We help you understand whether and how the 30% ITC applies to your situation before you commit to a financing structure.

- Side-by-side financing comparison. We show you what each option looks like on a monthly basis, over the loan or lease term, and over the full 25-year system life so you can make a decision based on real numbers.

- No pressure. If a lease makes more sense for your situation than a loan, we will tell you that. The goal is to find the right fit, not to close a deal.

The best solar financing option depends on your goals, budget, and long-term plans. At 8MSolar, we will walk you through every option and help you choose the solution that makes the most sense for your home. Schedule a free solar consultation today.

Frequently Asked Questions

Is a solar loan better than a solar lease?

For most homeowners seeking maximum long-term savings and ownership benefits, a solar loan is the stronger financial choice. However, leases can be a better fit for homeowners who prioritize low upfront cost, simplicity, or who have limited tax liability to offset with the federal tax credit.

Do I own my solar panels with a solar lease?

No. With a solar lease, the leasing company owns the panels. You are paying for the right to use the energy they produce. Ownership transfers to you only if you purchase the system at the end of the lease term, which some agreements allow.

Who gets the solar tax credit with a lease?

The leasing company claims the 30% federal Investment Tax Credit because they own the system. Homeowners who want to capture this incentive need to own their system through a loan or cash purchase.

Can a solar lease increase home value?

Research suggests that owned solar systems increase home value. The impact of a leased system is less clear and can complicate the sale process if the buyer is unwilling to assume the lease obligation.

What happens if I sell my home?

With an owned system, the solar installation transfers with the home like any other fixture. With a lease, you must either transfer the lease to the buyer or pay a buyout fee to terminate the lease early. Some buyers are comfortable assuming a lease; others are not.

What is a prepaid solar lease?

A prepaid solar lease is a lump-sum payment made upfront to cover the full lease term, eliminating monthly payments. The leasing company still owns the system and claims the tax credit, but the homeowner has no ongoing payment obligation for the lease period.

Are solar loans worth it?

For most NC homeowners with adequate sun exposure and electricity usage above $100 per month, yes. The combination of the 30% federal tax credit, rising utility rates, and a 25-year system lifespan makes a well-structured solar loan a strong long-term investment.

What is the cheapest way to finance solar?

Cash purchase produces the lowest total cost over the system’s life because there is no interest to pay. For homeowners who do not want to deploy that much capital, a low-interest solar loan is typically the next most cost-effective option. Lease programs offer lower upfront costs but higher total payments over time.