Yes. Many North Carolina homeowners can install solar panels with little or no upfront cost through financing options such as solar loans, leases, and power purchase agreements. These programs allow you to start using solar energy without paying the full system cost upfront, though monthly payments and contract terms vary by financing option.

The important thing to understand is that “no money down” does not mean the system is free. It means the cost is structured differently. Instead of a large upfront payment, you make monthly payments over time. How those payments are structured, who owns the system, and what you walk away with at the end varies significantly depending on which financing path you choose.

This guide explains how each option works, what the real costs and benefits are, and how to determine which path makes the most sense for your home and financial goals.

The Short Answer: Can You Get Solar Panels With No Money Down?

Yes, in most cases. The most common no-money-down solar options are:

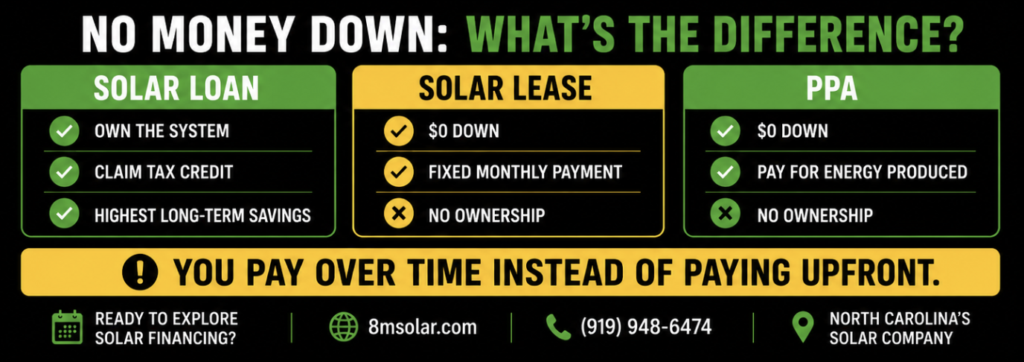

- Solar loans: You borrow money to purchase the system, own it outright, and repay the loan monthly.

- Solar leases: A third party owns the system and installs it on your roof; you pay a monthly lease payment to use the energy it produces.

- Power Purchase Agreements (PPAs): Similar to a lease, but you pay per kilowatt-hour of energy produced rather than a fixed monthly amount.

Each of these options has different implications for ownership, long-term savings, and what happens if you sell your home. Understanding those differences before choosing is more important than finding the lowest monthly number.

What Does “No Money Down Solar” Actually Mean?

When a solar company advertises no money down, it means you do not need to pay the full system cost upfront to get started. You still pay for the system, just over time through monthly financing payments or lease payments rather than a single large check at signing.

It is worth clearing up a common misconception: there is no such thing as a truly free solar panel program for standard residential customers. Programs that advertise “free solar” are almost always describing a lease or PPA where someone else owns the system and you pay for the electricity it produces. The system is not given to you at no cost.

That distinction matters because it affects who owns the equipment on your roof, who claims the tax incentives, and how the long-term economics work out. A no-money-down loan and a no-money-down lease both start with zero dollars out of pocket, but they are very different financial arrangements.

No-Money-Down Solar Financing Options

Solar Loans

A solar loan is the most common no-money-down path for homeowners who want to own their system. You borrow the full cost of the system from a lender and repay it over a term typically ranging from 5 to 25 years. Current solar loan interest rates in 2025 range from approximately 4.5% to 9% depending on the lender, term length, and your credit profile.

Because you own the system, you are eligible for the 30% federal solar tax credit, which reduces your net system cost by 30% at tax time. Many homeowners use that tax credit to pay down their loan principal early, which reduces interest costs and shortens the payback period.

When structured correctly, the monthly loan payment is designed to be equal to or less than your current electricity bill, meaning you save money from month one. Once the loan is paid off, your electricity costs drop dramatically because the system is yours with no ongoing payment.

Solar Leases

Under a solar lease, a solar company installs panels on your roof and owns the equipment. You pay a fixed monthly lease payment in exchange for the right to use the energy the system produces. Programs like LightReach through Palmetto Solar are structured this way.

Lease payments are designed to be lower than your current electricity bill, so you see immediate savings. The company that owns the system handles maintenance and monitoring throughout the lease term, typically 20 to 25 years. At the end of the lease, you may have the option to purchase the system, renew the lease, or have it removed.

The tradeoff is that you do not own the system and do not claim the federal tax credit. That incentive goes to the leasing company as the system owner.

Power Purchase Agreements (PPAs)

A PPA is similar to a lease in that a third party owns the system and installs it on your roof at no upfront cost. The difference is in how you pay. Under a PPA, instead of a fixed monthly lease payment, you pay per kilowatt-hour for the energy the system produces, typically at a rate below your utility’s retail rate.

This means your monthly payment fluctuates with system production. In high-production months, you may use more solar energy and pay more to the PPA provider, but your total energy costs are still lower than they would have been without solar. In low-production months, the payment drops accordingly.

Like a lease, the system owner claims the federal tax credit under a PPA, not the homeowner.

Prepaid Solar Leases

A prepaid solar lease is a variation where instead of making monthly payments over the lease term, you pay a single lump sum upfront to cover the full lease period. This eliminates ongoing monthly payments while still operating under a third-party ownership structure.

Prepaid leases can make sense for homeowners who have capital available but do not want to purchase the system outright, or who prefer to avoid monthly billing. The system still belongs to the leasing company, and the tax credit still goes to them. Whether a prepaid lease makes financial sense compared to an outright purchase or a loan depends on the specific terms and your tax situation.

What Are the Advantages of No-Money-Down Solar?

Lower Upfront Cost

The most obvious benefit is accessibility. Most homeowners do not have $20,000 to $35,000 sitting available to purchase a solar system outright. No-money-down financing makes solar possible for households that want the benefits of solar energy without depleting savings or home equity.

Immediate Energy Savings

Whether you choose a loan or a lease, no-money-down solar is typically structured so that your monthly payment is lower than your current electricity bill. That means you start saving money from the first month, even while you are still making payments on the system.

Access to Solar for More Homeowners

Financing options have opened solar to a much broader range of households. Homeowners who were previously priced out of solar because of high upfront costs can now access the technology and begin reducing their electricity bills and carbon footprint.

Preserve Cash for Other Priorities

Even homeowners who could pay cash for a solar system sometimes choose financing because it allows them to keep their capital available for other investments or needs. A low-interest solar loan that pays for itself through energy savings can be a more efficient use of capital than tying up a large sum in home infrastructure.

Are There Any Downsides?

Monthly Payment Obligations

No-money-down financing means monthly obligations. If your financial situation changes and you need to reduce expenses, a solar loan or lease payment is a fixed commitment that does not flex easily.

Interest Costs

Solar loans carry interest, which means you pay more than the sticker price of the system over the loan term. The total interest paid depends on your rate and term length. Lower interest rates and shorter terms reduce this cost, but it is a real factor in the total cost of ownership.

Ownership Limitations With Leases

With a lease or PPA, you do not own the system and do not claim the federal tax credit. The long-term savings potential is lower than with ownership because you are still making payments throughout the lease period rather than reaching a payoff point after which your energy is effectively free.

Contract Terms

Lease and PPA agreements are long-term contracts, typically 20 to 25 years. Some include annual payment escalators where your monthly payment increases slightly each year. Always review the full terms of any agreement before signing, including escalator clauses and early termination provisions.

Selling Your Home

An owned solar system transfers with the home like any other fixture and generally adds to home value. A leased system requires either transferring the lease to the buyer or paying a buyout to terminate the lease early. Some buyers are comfortable assuming a lease; others are not, which can complicate a sale.

How Much Can Homeowners Save With No-Money-Down Solar?

Actual savings depend on your energy usage, utility rates, system size, and financing terms, but here is a realistic picture for NC homeowners:

| Financing Option | Upfront Cost | Who Owns System | Tax Credit | Typical Monthly Impact | Long-Term Savings |

| Cash Purchase | Full system cost | You | You claim it | Full savings from day one | Highest |

| Solar Loan | None | You | You claim it | Net positive from month one | High |

| Solar Lease | None | Leasing company | Leasing company | Lower bill from month one | Moderate |

| PPA | None | PPA company | PPA company | Lower per-kWh rate | Moderate |

| Prepaid Lease | Lump sum (below purchase cost) | Leasing company | Leasing company | No monthly payment | Moderate |

For a typical NC family home with a $175 monthly electric bill, a no-money-down solar loan might produce estimated annual savings of $1,400 to $1,900 after loan payments, rising over time as utility rates increase. A lease might produce immediate monthly savings of $30 to $80 depending on the payment structure, with less total savings over 25 years because payments continue throughout the lease term.

These are illustrative estimates. Your actual savings depend on your specific energy usage, roof conditions, Duke Energy solar programs and rates, and the exact terms of your financing agreement.

Is No-Money-Down Solar Worth It?

Homeowners Planning to Stay Long-Term

For homeowners who plan to stay in their home for 10 or more years, a no-money-down loan is typically the strongest financial choice. The combination of the tax credit, rising utility rates, and the post-payoff savings period creates a compelling long-term return. Review your estimated solar payback period as part of your decision.

Homeowners Focused on Cash Flow

If your primary goal is reducing your monthly electricity bill immediately with the simplest possible arrangement, a lease or PPA accomplishes that with minimal complexity. You will not maximize your long-term return, but you will reduce your energy costs from month one without qualifying for a loan or managing a tax credit.

Homeowners Looking for Energy Independence

Solar paired with battery storage solutions provides resilience against grid outages and rising utility rates regardless of which financing structure you choose. For homeowners who experienced extended outages during storms or who are concerned about grid reliability, the energy independence value of solar and battery adds a meaningful non-financial dimension to the decision.

How 8MSolar Helps Homeowners Explore Financing Options

At 8MSolar, we offer solar financing options including loans, cash purchase, and lease programs for NC homeowners. We do not push one financing path over another. Our job is to help you understand what each option actually means for your situation and make the choice that fits your goals.

Here is how we approach the conversation:

- We start with your energy data. Before we talk about financing, we look at your actual electricity usage and roof conditions to understand what size system makes sense for your home.

- We model multiple scenarios. We show you what a loan, a lease, and a cash purchase look like side by side, including monthly payments, tax credit implications, and 25-year savings estimates.

- We explain the details. We walk through contract terms, escalator clauses, ownership implications, and what happens if you sell your home. No surprises after you sign.

- We give you a straight recommendation. Based on your goals and financial situation, we tell you which option we think makes the most sense and why.

Solar is more accessible today than it has ever been. Whether you are interested in a loan, lease, or another financing option, 8MSolar can help you compare your choices and determine what makes the most sense for your home and budget. Schedule your free solar consultation today.

Frequently Asked Questions

Can I really get solar panels with no money down?

Yes. Solar loans, leases, and PPAs all allow homeowners to go solar without a large upfront payment. Monthly payments vary by financing option and system size. The system is not free, but the cost is spread over time rather than paid upfront.

Is no-money-down solar a scam?

No, but the phrase is sometimes used misleadingly. No-money-down solar refers to financing arrangements where you pay over time rather than upfront. Legitimate programs from established lenders and leasing companies are widely available. The key is understanding the full terms of any agreement before signing, including interest rates, escalator clauses, and contract length.

Do I own the solar panels with a no-money-down program?

It depends on the financing type. With a solar loan, you own the system from day one. With a lease or PPA, the third-party company owns the system throughout the contract period.

What credit score do I need for solar financing?

Requirements vary by lender and financing type. Most solar loans require a minimum credit score of approximately 640 to 700. Lease programs like LightReach typically require a minimum 660 FICO score with no strict debt-to-income requirements, making them more accessible for some homeowners.

Is a solar loan better than a solar lease?

For most homeowners seeking maximum long-term savings and ownership benefits, a loan is generally the stronger option. Leases work better for homeowners who prioritize simplicity, have limited tax liability, or prefer not to take on a financing obligation. Read our full solar lease vs. solar loan guide for a detailed comparison.

Can no-money-down solar lower my electric bill immediately?

In most cases, yes. Both loans and leases are structured so that monthly payments are lower than the electricity costs the system offsets. Most NC homeowners see a net positive impact on their monthly expenses from the first month.

What happens if I sell my house?

With an owned system via a loan, the solar installation transfers with the home like any other fixture. With a lease or PPA, you must transfer the lease to the buyer or pay a buyout fee. Most experienced real estate agents in NC are familiar with solar transfers, but a leased system can add a step to the sales process.

Are there no-money-down solar options in North Carolina?

Yes. 8MSolar offers solar loans, lease programs, and cash purchase options for NC homeowners. Multiple financing programs are available depending on your credit profile, energy usage, and goals. Contact our team to review what is available for your specific situation.