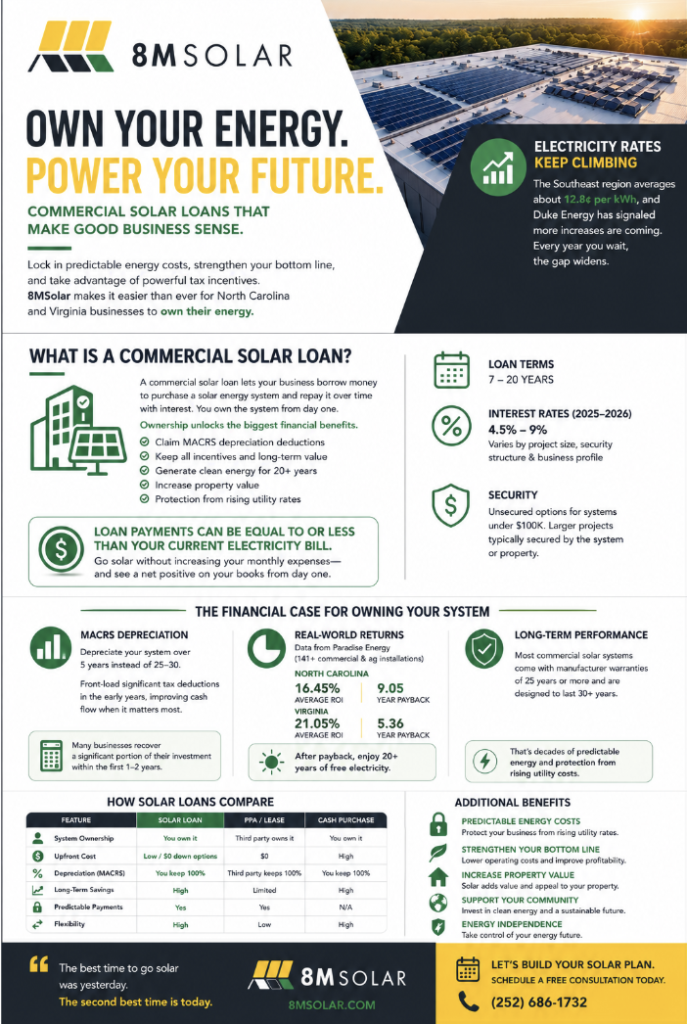

Your electricity bill is one of your most predictable operating costs, until it isn’t. Across North Carolina, commercial electricity rates have been climbing, and businesses that locked in their energy costs through solar a few years ago are watching their competitors scramble to absorb rate hikes that keep coming. The Southeast region currently averages about 12.8 cents per kilowatt-hour, but that number isn’t sitting still. Duke Energy has already signaled more increases are coming, and every year you wait, the gap between what you’re paying now and what you could be paying widens.

For many business owners, the biggest barrier to going solar has always been the cost. A commercial solar system is a big investment, no question about it. But that’s exactly where commercial solar loans change the math. Instead of paying a lump sum, you finance the system and start saving money from day one, because your loan payment can be less than your current energy bill. You keep your capital, your cash flow stays intact, and you still walk away owning the system outright.

This guide covers how commercial solar loans work, what financial benefits they unlock, how they compare to other financing options, and what North Carolina business owners need to know before signing anything. 8MSolar now offers commercial solar loans, making it easier than ever for local businesses to own their energy and put an end to unpredictable utility bills.

What Is a Commercial Solar Loan?

A commercial solar loan works the same way as most business financing: you borrow money to purchase a solar energy system, then repay the loan over time with interest. The system is yours from day one. That’s the main distinction between a loan and other solar financing options like power purchase agreements (PPAs) or leases, where a third party owns the equipment and you’re simply a customer paying for the output.

Ownership is what unlocks the biggest financial benefits. When your business owns the solar system, you qualify for depreciation deductions under the Modified Accelerated Cost Recovery System (MACRS). This tax incentive can return a huge portion of your investment within the first year or two, shortening the payback period. A business that finances through a PPA or lease hands those benefits to the system owner instead.

Loan terms for commercial solar usually run from 7 to 20 years. Current interest rates in 2026 range from about 4.5% to 9%, depending on the size of the project, the security structure, and your business’s financial profile. Smaller systems under $100,000 may qualify for unsecured financing; larger projects are typically secured against the solar system itself or the property. For projects in rural areas, the USDA REAP program can provide loan guarantees that make financing more accessible.

The monthly loan payment structure is what makes commercial solar loans appealing for businesses watching their cash flow. When designed correctly, the loan payment is structured to be equal to or less than the electricity costs the system offsets, which means you can go solar without increasing your monthly expenses. In many cases, businesses see a net positive on their books from month one.

The Financial Case for Owning Your System

MACRS Depreciation

MACRS (Modified Accelerated Cost Recovery System) allows commercial solar owners to depreciate the value of their system over five years rather than the full useful life of 25 to 30 years. This front-loads significant tax deductions in the early years of ownership, improving cash flow when it matters most. Combined with the ITC and bonus depreciation, many businesses can recover well over 50% of their system’s cost within the first one to two years through tax savings alone.

It’s worth talking with your CPA before installation to model exactly how these incentives apply to your business’s tax situation. The timing and structure of your project can affect how much you recover and when. An experienced solar installer, one with engineers who have worked through hundreds of commercial projects, can help you coordinate that conversation.

Real-World Returns

The numbers back this up. According to data from Paradise Energy, which analyzed over 141 commercial and agricultural solar installations, the average ROI for commercial solar is 16.45%, with an average payback period of 9.05 years.

Most commercial solar systems also come with manufacturer warranties of 25 years or more. The investment that pays itself back in under a decade then keeps producing returns for decades after. That’s not a short-term financial decision. It’s a long-term asset that works for your business every single day.

How Commercial Solar Loans Compare to Other Options

There are a few ways to finance commercial solar, and they aren’t all equal. Here’s a straightforward comparison:

| Financing Option | You Own the System? | Claim Tax Incentives? | Upfront Cost | Long-Term Savings |

| Cash Purchase | Yes | Yes | High | Highest |

| Solar Loan | Yes | Yes | Low | High |

| Power Purchase Agreement (PPA) | No | No | None | Moderate |

| Solar Lease | No | No | Low | Lower |

A cash purchase gives you the best total return because there’s no interest to pay. But most businesses would rather keep capital working in their operations rather than tie it up in infrastructure. A solar loan is the practical middle ground: you get full ownership and all tax benefits, with manageable monthly payments instead of a large upfront outlay.

PPAs and leases remove the ownership burden, but they also remove the upside. You don’t claim the ITC. You don’t get the depreciation. And because a third party owns the system, the financial benefits accrue to them, not you. You’re also locked into a long-term contract with another company managing equipment on your property. For businesses that want to maximize the return on their solar investment and maintain control of their energy infrastructure, a loan is the clear choice.

What to Expect During the Loan Process

Getting a commercial solar loan is straightforward, especially when you’re working with an experienced installer who understands the technical and financial side of the project. The process shouldn’t feel like navigating a bank on your own. A good installation partner walks you through every step.

Here’s how it works:

- Energy assessment: Your 8MSolar engineer reviews your facility’s electricity usage, roof or ground space, and grid connection to design a system sized for your actual needs, not a one-size-fits-all estimate.

- Financial modeling: We calculate the projected savings, payback period, and how the ITC and depreciation apply to your specific tax situation, so you know exactly what to expect before committing.

- Loan application: We connect you with financing options that fit your project size and timeline. Loan terms, interest rates, and payment structures are reviewed with you before anything is signed.

- Installation: 8MSolar’s in-house engineering team handles permitting, installation, and utility interconnection. You don’t manage subcontractors or coordinate between multiple vendors.

- Monitoring: After installation, your system’s output is tracked so you can see exactly how much energy you’re producing and how much you’re saving, month by month.

The timeline from initial consultation to a producing system varies by project size, but most commercial installations move from signed contract to operational within a few months. Permitting timelines vary by county in North Carolina, and our team is experienced navigating them.

What Businesses Qualify?

Commercial solar loans are available to a wide range of business types and property owners. If your facility uses a meaningful amount of electricity and you own or have long-term control of the roof or land, you’re likely a candidate. The most common applicants include:

- Office buildings and professional services firms

- Retail centers and shopping complexes

- Warehouses and distribution centers

- Manufacturing and industrial facilities

- Agricultural operations and farms

- Nonprofits and religious institutions

The USDA Rural Energy for America Program (REAP) offers an additional layer of financing specifically for rural small businesses and agricultural producers. REAP provides loan guarantees on up to 75% of eligible project costs, plus grants covering up to 25% of total costs. These benefits can be stacked with the 30% solar ITC, making commercial solar extremely affordable for farms and rural operations across eastern North Carolina.

Lenders evaluate commercial solar loans based on system size, projected energy production, ownership structure, and the borrower’s overall financial profile. Credit requirements vary, but this is not a consumer loan process. It’s structured around the project’s performance and the business behind it. For businesses with strong financials and clear energy usage data, approval is generally straightforward. Lenders in the commercial solar space understand the asset well. A properly designed system in a strong sun market like North Carolina or Virginia is a predictable, bankable investment.

The size of your system matters too. Systems under $100,000 can qualify for unsecured lending, which simplifies the process considerably. Larger projects are typically secured against the solar asset or the underlying property, and for the biggest installations, C-PACE financing (Commercial Property Assessed Clean Energy) is another option worth discussing with your installer. C-PACE allows businesses to repay the loan through a property tax assessment, which can offer longer terms and favorable rates for qualifying projects.

For businesses that don’t fit neatly into standard financing options, it helps to work with an installer who can model the full picture and advocate for you in the process, not just hand you a brochure and point you toward a lender.

What Solar Loans Mean for Energy Costs Long Term

Here’s the piece of the conversation that most financing guides leave out: electricity rates aren’t static, and that fact works in your favor once you own a solar system. The national average for commercial electricity in the Southeast was around 12.8 cents per kilowatt-hour in 2025, but utility rates have been climbing year over year. Duke Energy’s recent rate increases are a clear signal of where things are headed, and there’s no reason to expect that trend to reverse.

When your business finances a solar system with a fixed-rate loan, your energy cost for the electricity that system produces is locked in for the life of the loan. The solar panels don’t charge more because the grid got expensive. Every rate increase from your utility makes your solar investment more valuable, not less. Businesses that went solar five years ago aren’t just saving money on their current bill. They’re saving more with every rate hike that passes them by.

Beyond rate protection, owning a solar system can also improve your property’s value and strengthen your business’s sustainability profile. More commercial tenants, customers, and partners are factoring environmental responsibility into their decisions. A solar installation is a visible, verifiable commitment, one that shows up on your roof and on your balance sheet. It also creates a layer of energy resilience that traditional grid dependence simply doesn’t offer. When the grid goes down during a storm or a peak demand event, businesses with solar and battery backup keep operating while others wait.

Over a 25 to 30-year system lifespan, the financial protection against rising rates, combined with the energy resilience, environmental credibility, and property value gains, can create a lasting strategic advantage for your business. The companies that made this decision five years ago aren’t second-guessing it. They’re renewing leases, expanding their systems, and watching their energy costs stay flat while everyone else’s climbs.

Stop Renting Your Electricity. Start Owning It.

The financial case for commercial solar has never been stronger. Bonus depreciation sits at 40% in 2026 and drops every year after. Duke Energy rates are rising in North Carolina. And with a commercial solar loan, you don’t have to write a large check to get started. You can own your system, claim every tax benefit, and begin saving from the first month.

8MSolar now offers commercial solar loans for businesses across North Carolina and Virginia. Our in-house engineering team will design a system matched to your facility, walk you through every financing option, and handle everything from permitting to installation to long-term monitoring. We’ve been doing this for over two decades, we’re NABCEP certified, and we’re not going anywhere.

Call us today at (919) 948-6474 or reach out online to schedule your free consultation. Your competitors aren’t waiting, and neither should you.